Word on the street > A Manifesto for the AE Industry (Part 3); What Exactly Are Your Owners Owning?

Word on the Street: Issue 295

Weekly real-time market and industry intelligence from Morrissey Goodale firm leaders.

A Manifesto for the AE Industry (Part 3)

Over the past two weeks, our three-part manifesto has walked from the wide-angle State of the Industry (Part 1) through the record-setting wave of Consolidation and (Re)Capitalization reshaping who owns the industry (Part 2). Today we close with the topic that’s been hiding in plain sight the whole time—Artificial Intelligence.

Now the nuance—and there’s a lot of it. The technology changes monthly, which means nobody truly understands the long-term impacts yet (anyone who tells you otherwise is selling something). The returns are real but hard to measure. And the risks are just as real as the rewards. This is the most exciting—and most misunderstood—force in the industry today. And precisely because it’s so misunderstood, sitting on the sidelines isn’t the safe choice it looks like. As Rex White, Morrissey Goodale’s VP of Strategy, puts it: “In a technology that moves this fast, the edge isn’t having the answers. It’s being honest about what you don’t know—and moving anyway, eyes open.”

Where we are today:

- The technology changes monthly. We’re all building the plane, changing out the older engines with newer ones, and reading the owner’s manual while flying it through a storm while our co-pilot is taking a nap.

- Awareness and experimentation are widespread, and AI investment is rising—though the depth of adoption varies enormously from firm to firm.

- CEOs are mainly using AI to do lower-level tasks faster. The top uses today are internal documentation and efficiency, followed by proposals and marketing.

- Most of the return on AI sits in internal efficiency right now, not new revenue. Client-facing AI is only just emerging.

- Execution still lags the enthusiasm. Many firms are early in translating AI pilots into measurable financial impact, and the return on AI spend remains hard to quantify and mostly informal.

- The benefits have not yet shown up in firm valuations—which, for the strategically minded, is precisely where the opportunity lies (more on that below).

- The risk is real—part 1. The models can be confidently wrong on hard questions, and most AE insurers are planning AI-related rate increases. Judgment still matters—arguably more than ever.

- The risk is real—part 2. You (or at least eager beavers in your firm busy pasting their work into free chat tools) are giving away your IP.

Our outlook—The next 12 months:

- AI will stay primarily an efficiency play as firms work to grow revenue without adding headcount. (Yes—this is the thread we’ve been pulling since Part 1 of the trilogy. Here’s where it lands.)

- Early movers will begin turning client data services into genuinely new revenue streams, not just internal savings.

- Pricing will start shifting toward value-based and lump-sum models to capture AI-driven productivity—because if you bill by the hour and AI makes you 10 times faster, you’ve just penalized yourself for being good.

- You’ll have given away even more of your IP (despite your best efforts)—usage spreads faster than guardrails.

And over the next five years:

- AI will become a genuine long-term value driver as it’s more fully integrated into delivery, pricing, and client service. The value shows up first as efficiency, then as differentiation.

- Competition will shift from capacity to expertise, judgment, and trusted client relationships. When everyone has the same powerful tools, the differentiator is the human wielding them.

- Human judgment, experience, and licensure will remain the real differentiators. The engineer isn’t going away—the role is being rewritten.

- AI will reshape staffing, project delivery, and the very structure of the firm—and the long-term impact will depend entirely on how deeply it’s integrated into delivery rather than bolted on the side.

- Bye-bye, IP—unless you decide now, through strong policy and governance, what’s worth protecting.

And that closes the manifesto. Step back and look at all three parts together, and a single story emerges. The industry is strong (Part 1). Capital and consolidation are reshaping who owns it (Part 2). And AI is quietly reshaping how it creates value in the first place (Part 3). These aren’t three separate stories—they’re one. The firms that will define the next decade are the ones that see the connection: that leadership transition, capital strategy, and technology are now a single, integrated strategic conversation. The Golden Age for the AE industry isn’t over. But it belongs, from here on out, to the firms bold enough to write the new rules rather than wait to read them.

Here’s a prediction worth acting on: The value AI creates hasn’t shown up in firm valuations yet—but it will, and the deal market will be the first place you see it. Come pressure-test that thesis with over 140 AE industry CEOs, corporate development executives, and investors at The M&A and Capitalization Symposium in Houston this October. It’s where the conversations about capital, consolidation, and the technology driving the next wave of value all happen in the same room, in one of the nation’s fastest-growing cities. Early-bird registration closes July 31—register now and save.

To connect with Mick, email him at [email protected].

What Exactly Are Your Owners Owning?

Walk into almost any AE firm and ask the owners what they worked on over the past two weeks. You’ll hear about projects that needed rescuing, proposals that had to go out, difficult clients, staffing problems, collections, contract language, recruiting, utilization, and probably at least one software issue that somehow became a leadership priority.

None of those things are unimportant. In fact, many of them are essential. The problem is that when you compare that list to the handful of things the firm actually needs its owners to accomplish, the overlap is often surprisingly small.

That isn’t because the owners are lazy or disengaged. Quite the opposite. Most are working incredibly hard. They’re just working on the wrong things. It’s one of the most common patterns we see during strategic planning engagements. Firms promote talented technical professionals into ownership, but they rarely redefine what success looks like after they become owners. The expectations simply continue to evolve on their own. Before long, everyone is busy, everyone is overloaded, and very little owner time is being invested in building the firm’s future. The owners are running the business, but too few are actually working on owning it.

Ownership changes the compensation more than the job…

Most firms are very deliberate about deciding who should become an owner. They spend years evaluating technical ability, client relationships, leadership potential, and commitment to the firm. They debate candidates carefully before offering equity. What they are often far less deliberate about is defining what the person’s job becomes after the stock certificate changes hands.

New owners usually continue doing exactly what made them successful before becoming owners. They run projects, supervise staff, solve client problems, review proposals, and jump into operational issues whenever needed. None of those activities are unimportant, but they are largely the same activities they performed before joining the ownership group. So, the compensation changed, but the expectations did not.

Try this…

There is a simple exercise that can be revealing, and occasionally a little uncomfortable. Ask your owners to track their activities for two weeks. Simply write them down—every phone call, meeting, or interruption. By the end of two weeks, a typical list will look something like:

- Red-lining Joe’s plan because he wanted one more set of eyes on it

- Sitting in an emergency meeting about the Oak Street project

- Answering 47 emails, most of which probably didn’t require an owner’s involvement

- Helping negotiate a change order

- Chasing down a subconsultant

- Reviewing invoices

- Sitting through internal meetings that accomplished little beyond scheduling another meeting

- Solving a staffing problem that someone else should eventually be able to solve

- Reviewing a proposal because “you’ve always reviewed the big ones”

- Taking a client call that really should have been handled by the project manager

- Approving expenses

- Tweaking a PowerPoint presentation

- Helping put out another fire that somehow became your fire

Now compare the two lists. If an owner spends fifty hours over two weeks solving project issues and two hours mentoring future leaders, you can put your finger on the issue(s).

As you can clearly see, operational work has a remarkable ability to expand until it fills every available hour. There is always another project deadline, client issue, proposal, staffing problem, invoice, or emergency meeting demanding an owner’s attention. And they are all immediate.

Strategic work operates differently. The consequences of putting it off are rarely felt today, which is why it is so often pushed aside. Over time, however, the cost becomes evident. Recruiting gets harder, the leadership bench gets thinner, growth slows, and competitors begin pulling ahead. Those problems rarely start when they become visible. More often, they begin years earlier, when owners gradually allowed the urgent work of running the business to crowd out the important work of building it.

Don’t make this mistake…

A common mistake is trying to define ownership with a single job description. The ownership group should absolutely share common expectations, but that doesn’t mean every owner should contribute in the same way. One owner may excel at opening doors with major clients, another at recruiting top talent, another at mentoring future leaders, and another at identifying acquisition opportunities or new markets.

The important question is not whether every owner performs the same role, but whether every owner has a clearly defined enterprise responsibility that extends beyond running projects or managing a department. A useful question during strategic planning is this: “If this owner disappeared for six months, what critical firm-wide capability would we lose?” If the answer is simply, “We’d have to find a way to manage a lot of projects,” the ownership role probably hasn’t evolved as much as it should.

The big trap…

One of the biggest reasons owners stay trapped in operations is that, in many cases, they really are the best person to handle the issue. They can solve the problem faster, make the decision more confidently, or rescue a struggling project more effectively than anyone else. The trouble is that if every important decision still depends on an owner, leadership development stalls out and the bench gets thin.

Owners tell me every week, if not every day, that they don’t have time to mentor because they’re too busy doing the work. More often than not, it’s the opposite that’s true. They’re too busy doing the work because they haven’t invested enough time in developing people who can eventually do it themselves. Firms don’t grow from $20 million to $100 million because the owners become better firefighters. They grow because the owners gradually build leaders who can put out fires without them.

How clarity changes behavior…

One of the simplest improvements a leadership team can make is to clearly define what ownership means inside the firm (not philosophically, but operationally). If you asked every owner to write down their three most important enterprise responsibilities, would the answers be similar? Would the CEO agree with them? Would younger principals understand what success looks like once they become owners?

In many firms, the answers vary widely because those expectations have never been clearly established. When that happens, owners naturally gravitate toward work they understand, enjoy, and receive immediate feedback for. Projects check all three boxes. Building future competitive advantages usually checks none of them. Without clear expectations and accountability, owners gradually become senior project managers with stock certificates rather than owners focused on increasing the long-term value of the business.

The question to ask…

Technical excellence will always be at the heart of a successful AE firm. The question is whether owners are also investing enough time in the handful of responsibilities that only they can fulfill.

Market Snapshot: CNBC’s Top States for Business

Weekly market intelligence for AE and environmental industry leaders.

Buoyed by the country’s highest marks for infrastructure and cost of doing business, Ohio ranked first in CNBC’s 20th annual Top States for Business list released last week. The Buckeye State, which cracked the top five for the first time last year, has risen steadily after placing 30th in the business news network’s first competitiveness index in 2007.

Real estate data firm CoStar reports that Ohio’s office and industrial rental rates are among the country’s lowest, and relatively affordable housing costs contributed to the state ranking ninth in cost of living. According to Site Selectors Guild, the state boasts one of America’s most robust programs for pairing companies with shovel-ready development sites, with the $175 million earmarked for site readiness in 2025 trailing only California. The one blemish: With only 19% of residents possessing a bachelor’s degree or higher, according to the U.S. Census Bureau, Ohio ranked 35th in workforce.

Placing second on the list was North Carolina, which topped CNBC’s ranking last year and possessed the number one economy in this year’s study. Rounding out the top five were Virginia, whose second-place infrastructure rating was offset by federal budget and personnel cuts; Texas, which ranked first for workforce and second for economy and access to capital but 49th for quality of life; and Minnesota, whose fourth-place quality of life ranking was tempered by a high cost of living.

On the flip side, the two states outside the continental U.S. ranked at the bottom of CNBC’s list—with Hawaii in 50th and Alaska in 49th place. Rhode Island, Louisiana, and West Virginia rounded out the bottom five.

Arkansas made the list’s biggest leap, rising 13 spots to #28, with employers such as Walmart, Tyson Foods, and J.B. Hunt Transport Services attracting workers to the state’s northwest region. Other fast risers included Nevada, which jumped nine spots to #33, and Maine, which rose eight spots to #35. Colorado sustained the biggest drop, falling 14 spots to #25, while Nebraska dipped 11 places to #26 and South Dakota 9 spots to #44.

For questions about our market intelligence and research services, contact Rafael Barbosa.

Word on the Street Podcast Spotlight

Weekly M&A Round Up

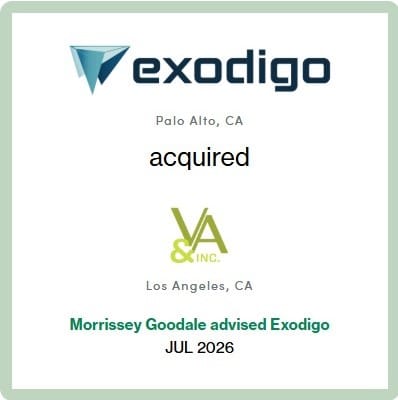

Congratulations to Exodigo (Palo Alto, CA): The subsurface intelligence and AI-engineering firm acquired V&A (Los Angeles, CA), a civil engineering firm that provides utility and traffic engineering services across transportation, aviation, water, energy, and infrastructure sectors. We feel privileged that the Exodigo team trusted us to advise them on this transaction.

18 deals reported last week, led by an AI-engineering featured transaction: Deal activity picked up last week, with eleven domestic transactions announced in CA, NC, GA, MN, AL, TN, TX, SC, and VA, while seven deals were reported internationally across Australia, Germany, Singapore, Portugal, and the UK. Exodigo’s acquisition of V&A highlights the continued convergence of AI and engineering services as technology-enabled platforms acquire traditional AE firms to expand delivery capabilities and embed technology directly into service offerings. Check out all of the week’s M&A news here.

The M&A and Capitalization Symposium

Learn what’s new (and next) in the world of AE M&A and Capitalization and make valuable new connections at the Post Oak Hotel at Uptown, Houston, TX.

The Top 5 M&A Questions CEOs Are Asking in 2026

Explore the five questions driving M&A strategy, valuation, and ownership decisions across the AE industry in 2026.

Keep Up to Date with

Industry Insights

Stay up-to-date in real-time.