Word on the street > Why It Pays to Be an Under-Performing Firm; SECTION 174-Having fun yet?

Word on the Street: Issue 145

Weekly real-time market and industry intelligence from Morrissey Goodale firm leaders.

Why It Pays to Be an Under-Performing Firm

My first business call after I got back from New Zealand last week was with the CEO of a long-time ENR 500 strategy client. “Mick, our Q1 gross revenues are up 50% over the same period last year, net revenues are up 40%, and profits are almost double.” His firm is coming off its third consecutive year of record financial performance. It has multiple years of backlog in-house with A-list clientele. His managers are turning down work. Sustaining this performance is his #1 priority. His nights of fitful sleep are filled with nightmares of project failures because his firm cannot find the staff to do the work. Sound familiar?

Great industry? Or the greatest industry? Bank failures. Record inflation. Highest interest rates in decades. Tech industry layoffs. Big deal. The AE industry shrugs all of these off and continues its decade of crushing it. At last month’s Southeast Symposium in Miami, we reported on an industry registering universally positive vital signs. Financial performance is humming (operating profits robust at 18%, staff utilization close to record highs at over 60%, overhead normalizing around 162%, and record net revenues per employee at close to $169,000). And balance sheets are stronger than ever with current ratios north of 4.0 and debt-to-equity ratios at a rock-bottom 0.46. Average backlog is close to a year’s worth of work. It’s no wonder that over 70% of the 200+ AE industry executives and investors attending the symposium were anticipating 2023 being an even better year for their firms than 2022. This June at our Western States Symposium in Las Vegas we’ll be sharing mid-year industry performance and outlook.

But wait, what’s this? However, not all indicators are “up.” And the direction of one in particular is downright confounding—the number of industry mergers. Traditionally, when the AE industry has experienced boom times, M&A has increased in line with the confidence of strategic acquirers and investors. But curiously, that’s not the case this year when the industry is arguably performing better than ever. The pace of consolidation in Q1 is actually down 25% over the same period last year, continuing a trend that we saw beginning in the middle of 2022. Indeed, M&A this year has fallen back to 2021 levels.

Knock-on effect: With this unexpected slowdown in M&A activity, it’s not surprising then that we’re seeing a corresponding softening in M&A multiples. The degree of value erosion varies depending on firm size and type. But to be sure (to be sure, for you Letterkenny fans) certain categories of firms are experiencing 10%+ declines from the highs of early 2022.

The (not so) curious case of under-performers: One category of firm that is bucking this valuation trend is that of the lower quartile of industry performers. These are the less-than-stellar firms. You know them. They are the ones whose websites look like they were created in 2012 and haven’t been updated in over a year. The firms that for whatever reason—mismanagement or bad luck—have flat-lining revenues or are seeing their profits erode and their backlogs dwindle. These firms—believe it or not—have seen their valuations increase by an average of 17% over the past year! Why?

Capacity—the most precious industry resource: This is what every successful industry firm is struggling to find in these boom times. And in 2023, that capacity still comes in the form of employees—be they in-office, hybrid, or remote. The 850,000 active professional engineers and 116,000 registered architects (thanks, ChatGPT) in the United States are just not enough to meet the current and anticipated demand for AE industry services. So, successful management teams continue to fine-tune their businesses to extract more performance from their existing staff, but this is a risky approach yielding diminishing returns while increasing the risk of burnout. They’re throwing money at internal and external recruiters only to pay top dollar to bring on board talent that they needed over a year ago. Too slow, too expensive.

A rising tide…: And this is why under-performing firms have seen an uptick in their valuations. Under-performing firms represent a rich, untapped vein of capacity. Unlike their high-performing peers, these firms tend to have lower firmwide utilization rates, with a ton of excess capacity available. In most cases these under-utilized staff are more than eager to take on the career-reaffirming opportunities presented to them by being part of a high-performing firm. So, buyers are targeting these under-performing firms as a way to quickly bring on board talent that can add capacity. And while they are not paying the multiples that they would for targets that allow them to meet strategic growth goals, they are paying relatively more than they did in the past—17% more—to quickly acquire the capacity that under-performers provide them that they cannot find elsewhere.

Questions, comments? Contact Mick @ [email protected] or 508.380.1868.

Section 174—Having Fun Yet?

We’ve been getting buried with inquiries from concerned AE firm leaders about Section 174, the rules of which require businesses to capitalize and amortize specified R&D expenditures over a period of five years.

To dig into some of the details, I spoke with Mike Woeber, CEO and president of Corporate Tax Advisors, Inc., a Huntsville, Alabama-based tax advisory firm that specializes in research and development tax credits. Here’s how it went:

![]()

Mike, thanks for talking with Word on the Street about this issue. It’s worrying many folks in the AE industry.

![]()

I can see why. It’s real money, and these are unchartered waters.

![]()

For starters, can you give an overview of Section 174?

![]()

Sure. The Tax Cuts and Jobs Act (TCJA), passed in December 2017, created a lot of advantages for taxpayers, including a reduction in the maximum corporate tax rate to 21%. While the tax savings were significant, it had to be paid for somehow. So, to get the plan through the Congressional Budget Office, Section 174 was amended to eliminate current-year deductibility of R&D costs beginning in 2022. Taxpayers must now charge those expenses to a capital account that would be amortized over five years.

![]()

This has to be a shock to the system.

![]()

Very much so. In the last four years, there have been a lot of efforts to overturn the revision, but things got increasingly contentious in Congress. We used to have a tax bill every other year, but we haven’t had one since 2019. There were other issues that needed addressing like COVID and climate change, and tax issues were largely ignored. It’s been five years since the TCJA passed, and now it’s on our doorstep and we have to deal with it on tax day.

![]()

How have firms been tracking R&D expenses?

![]()

In the past, the law said if you had an R&D expense—it didn’t matter what it was, whether it was a direct or indirect expense—it would be considered deductible. Because of that, most businesses didn’t account for R&D costs at all—they didn’t classify them as R&D. They just lumped everything in together because it was deductible anyway. It’s been the practice for the last 20 years, and suddenly you can’t deduct a block of expenses. Now it’s a scramble for firms to see what kind of information can be extracted from their systems.

![]()

Can firms still take the R&D credit?

![]()

Yes. The credit rules have not changed. Firms can still claim the credit they always have. It’s just the expenses that are not fully deductible in one year. So, the credit is still calculated the same way. The problem is that some firms will just say they don’t have any R&D expenses. But you can’t do that. You have to prove it. The public firms will comply because of SEC scrutiny around the tax provisions, but some small AE firms are taking a hard look at not taking the R&D credit because they figure they don’t have to add back any R&D expenses this year. But that’s a misread. Whether or not you take the credit, you have to account for R&D expenses. And that’s what’s getting people.

![]()

That sounds like a risky strategy.

![]()

It is. If firms had R&D expenses in the past and suddenly they don’t report any this year, they are playing the audit lottery. It’s probably not a good practice, and they could face penalties. It won’t give them any protection if they are audited. The other thing to worry about is you might be digging yourself a hole if you want to take the R&D credit in the future.

![]()

In addition to a higher tax burden, AE firms are now faced with the requirement of tracking their IRC Section 174 R&D costs. As you mentioned, many firms are not in the practice of tracking research costs since Section 174 previously allowed them to deduct R&D expenses in the year they were incurred. So now what?

![]()

If you have been taking the R&D credit, you have a basis for calculating the Section 174 adjustment. It’s primarily a wage-driven credit. Are you employing people who are doing innovative things? That’s the meat. But Section 174 goes further. For example, what’s the overhead, indirect labor, payroll taxes, and retirement that you are paying that’s not included in the R&D credit computation. Start with that labor then go back into indirect costs, and you can come up with a Section 174 expense. Now, different expenses qualify for the credit. Under Section 174, you must bring in the indirect costs. So, if your accounting system allows for it, you could set up an R&D cost center, but that creates a bit of an accounting nightmare. Instead, look at R&D labor and develop indirect cost allocations that relate to that R&D cost—the most defendable and relatable allocations. Some engineering firms will have DOT or state government requirements to create an overhead rate for billing cost-plus contracts. That would be way too high for R&D purposes, but it’s a template you could adapt for 174—if you are doing that overhead calculation anyway, you can adapt it for an R&D rate.

![]()

What are the chances this revision to Section 174 can be reversed, and do you think a reversal would be retroactive?

![]()

There is bipartisan support to have it done away with. But while the bill has been introduced, it has to get attached to a piece of legislation that actually has a chance of passing. Will it be retroactive? We’ll have to wait and see. The bill that came out a couple of weeks ago made it retroactive to January 1, 2022, which means it would completely disappear. The desire is to make it retroactive. Will it happen? We don’t know. But the proposals are to make it happen, and that’s encouraging. Some firms have decided to file extensions in the hope Congress will come to the rescue by mid- to late summer. It’s not a bad idea since there is so much focus on it right now. I still feel like it will get resolved, but in the meantime, firms are facing a hit of potentially millions of dollars, and that can be crippling.

Market Snapshot: K-12 Education (Part 1)

Weekly market intelligence data and insights for AE firm leaders.

Overview

- The K-12 education category of construction includes primary and secondary level of education institutions, which encompass elementary, middle and junior high, and high schools. It can also include academies, parochial, and vocational schools.

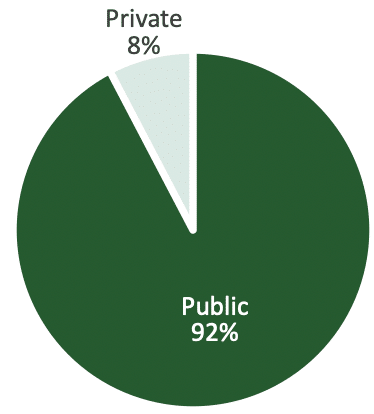

- Approximately 92% of the K-12 education construction spending comes from public-sector owners.

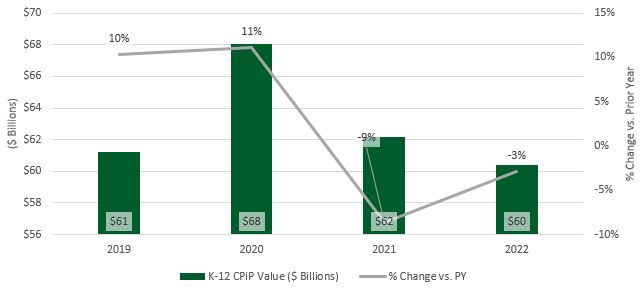

- According to the U.S. Census Bureau, total K-12 education construction spending was $60.4 billion in 2022, representing 67% of total education construction.

K-12 Education Market Breakdown

Market Size

$60.4 billion*

*Based on Value of Construction Put in Place (CPiP) – 2022 (U.S. Census Bureau)

K-12 Schools – Design and Construction Value

Outlook

- The overall K-12 education market for design and construction engineering has been decreasing since 2020, when construction spend reached $68 billion.

- The AIA Consensus Construction Forecast predicts 3% growth for education work in 2023.

- According to the National Center for Education Statistics (NCES), public and private enrollment is projected to decline at a rate of 0.8% per year until 2030. Projections from 2018 had enrollment for primary and secondary education reaching 57.39 million in 2028. The latest projection for the same year registers 52.58 million, which is most likely a reflection of the pandemic’s impact on the sector.

- High school graduation rates have continued on pace. Enrollment declines appear to be an impact felt mostly by primary grades in the short-term. Consequently, secondary and post-secondary education enrollment will be affected in future years.

- The American Society of Civil Engineers (ASCE), which grades school infrastructure with a ‘D+’, estimates that over half of the schools in the country need to update or replace building systems.

- Though the outlook for enrollment looks less than stellar, it doesn’t mean that there won’t be investments in school infrastructure in the coming years.

- Project opportunities may arise supported by federal funding investments in energy efficiency, air quality, and safety in K-12 schools.

In next week’s issue, we’ll look at trends and hot spots for this sector. To learn what’s ahead for other markets, check out Morrissey Goodale’s 2023 Market Outlook for the AE Industry. Click here to access recording and materials.

To learn more about market intelligence and research from Morrissey Goodale, schedule an intro call with Rafael Barbosa. Connect with him on LinkedIn.

Weekly M&A Round Up

Slowdown continues: Last week we reported a total of five domestic transactions with consolidation taking place in Virginia, North Carolina, Maine, New York, and Illinois. Overseas we reported one new transaction in Denmark. You can check all the week’s M&A news here.

.

Searching for an external Board member?

Our Board of Directors candidate database has over one hundred current and former CEOs, executives, business strategists, and experts from both inside and outside the AE and Environmental Consulting industry who are interested in serving on Boards. Contact Tim Pettepit via email or call him directly at (617) 982-3829 for pricing and access to the database.

Are you interested in serving on an AE firm Board of Directors?

We have numerous clients that are seeking qualified industry executives to serve on their boards. If you’re interested, please upload your resume here.

June 12-14, 2024 Las Vegas, NV

Western States M&A and Business Symposium

Join us for the 10th annual Western States Symposium, bringing together over 200 AE and environmental industry executives and investors in one of the world’s most vibrant and iconic cities.

Learn More

Subscribe to our Newsletters

Stay up-to-date in real-time.